Solving the Isolated AI Illusion in B2B Payment Recovery

You log into Stripe, see a 12% failed payment rate, and instantly click the toggle for Smart Retries. The dashboard promises machine learning will optimise recovery. Over in GoCardless, you enable Success+ to intelligently retry direct debits. You close the tab, assuming the AI has handled your involuntary churn.

Here is what actually happens.

Your payment processor starts playing a silent game of ping-pong with your customer's bank. Meanwhile, your Xero ledger shows an overdue invoice, your HubSpot CRM thinks the customer is perfectly healthy, and your automated onboarding emails keep firing.

The AI is working, but it is working in a vacuum. By the time the final retry fails 14 days later, the customer has churned, and nobody on your team knew they were at risk.

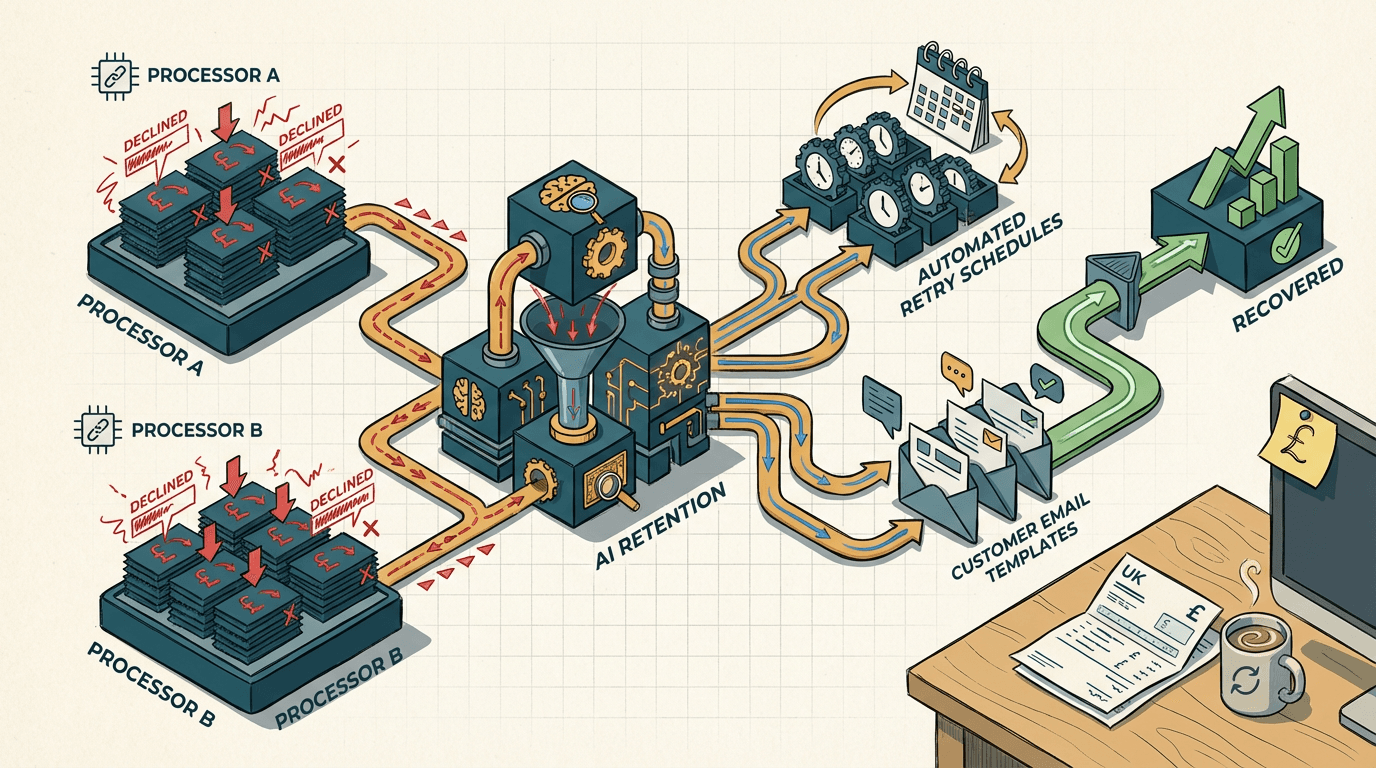

The isolated AI illusion

The isolated AI illusion is the false belief that toggling on a payment processor's smart retry feature will fix your involuntary churn without updating your underlying accounting and CRM systems.

It happens because founders treat billing as a single event. It isn't. Billing is a state machine. When a SaaS subscription payment fails, Stripe and GoCardless intercept the failure and use massive datasets to predict the best time to try again.

Stripe recovers about 57% of failed recurring card payments [source](https://stripe.com/billing/revenue-recovery), while GoCardless claims over 70% recovery for bank payments [source](https://gocardless.com/solutions/success-plus/).

Those numbers sound great. But they hide a structural mess.

While the AI waits for the optimal Tuesday afternoon to retry the charge, your operational stack is frozen in the past. The payment gateway knows the payment is pending retry, but it doesn't tell anyone else.

This affects every B2B SME relying on standard integrations. The ops manager assumes the native sync between Stripe and Xero handles everything. It doesn't. Native integrations only sync terminal states: paid or failed. They do not sync the liminal state of AI actively trying to recover funds.

The result is pure chaos. Your credit control software sends an aggressive dunning email to a client whose payment is already scheduled for an AI retry. Your sales rep calls them to pitch an upgrade. The AI is doing its job, but the business is completely blind to it.

Why the obvious fix fails

The obvious fix fails because standard automation tools cannot handle the nested data structures of an active AI retry schedule.

Most SMEs try to solve this by building a Zapier flow. They set a trigger for a failed payment in Stripe or GoCardless, and map it to an action that updates a contact property in HubSpot or a field in Xero. It seems logical.

It breaks almost immediately. Zapier's Find steps cannot nest deeply enough to parse the context of an AI retry. When a Stripe Smart Retry fails, the webhook payload is complex. The original invoice ID and the retry attempt count are buried three levels deep in the JSON object.

Zapier looks for the top-level ID, finds nothing, and silently writes a null value to your CRM. You only notice at month-end when reconciling accounts.

There is a contrarian reality here. You do not want your payment processor managing your customer communication. Stripe and GoCardless are exceptional at moving money. They are terrible at nuanced client relationships.

If you rely on their default dunning emails, your clients receive a robotic notice from a generic domain. It lacks context. It ignores whether they are a VIP client who has been with you for three years or a new signup on a starter tier.

In my experience auditing B2B billing stacks, most SMEs who rely on native Zapier integrations for churn recovery hit the same wall. The automation triggers at the wrong time, sends the wrong message, and fails to update the core ledger. You end up with a high recovery rate on paper, but a furious customer base and a broken Xero reconciliation.

The orchestration approach that actually works

To actually fix this, you need an orchestration layer that sits between your payment processor's AI and your operational stack.

You let Stripe or GoCardless handle the algorithmic retries, but you take control of the state management and the communication.

Here is a worked example of how you build this.

When GoCardless Success+ schedules a retry, it fires a webhook. An n8n workflow catches this payload. It extracts the customer ID and immediately updates a custom column in Xero called Dunning Status to reflect the active retry. It also flips a toggle in HubSpot to pause any automated marketing emails.

If the final AI retry fails, n8n does not just send a generic alert. It triggers an API call to Claude 3.5 Sonnet. Claude looks at the HubSpot record, sees the client's usage tier, and drafts a highly contextual, plain-text email sent directly from the account manager's Gmail via API.

The client replies. Often, in B2B SaaS, they reply with an attachment.

Let's say the input is an email subject line reading "RE: Account #492 - Updated Payment Details" and a PDF from supplier X explaining a new vendor portal process.

The n8n webhook catches this inbound email. It strips the email subject line and the PDF, sending both to Claude with a strict JSON schema. The prompt instructs Claude to extract the expected payment date and the new AP contact.

Claude parses the PDF, returns the structured JSON, and the n8n webhook PATCHes the Xero invoice line items with the new expected date. It updates the HubSpot record and drops a Slack message to the account manager confirming the new timeline.

This system takes 2-3 weeks to build. Expect it to cost £6k-£12k depending on how messy your existing Xero and HubSpot data is.

The main failure mode here is LLM hallucination. Claude might read a generic out-of-office auto-reply and invent a payment date. You catch this by enforcing the JSON schema. If the extracted date is more than 30 days in the future, or if the confidence score is low, n8n skips the Xero update and routes the payload to a human review channel in Slack.

Where this breaks down

This architecture is highly effective for modern B2B SaaS, but it hits a wall if your payment inputs are analog or heavily fragmented.

If your invoices come in as scanned TIFFs from legacy accounting, you need OCR first, and the error rate jumps from 1% to ~12%. Claude struggles with low-resolution scans of handwritten remittance slips.

It also breaks down if you process payments through legacy BACS transfers where the reference numbers do not match your CRM records. GoCardless maps Direct Debit mandates cleanly to customer IDs. But if a client bypasses the mandate and pushes a manual bank transfer with a misspelled company name as the reference, the n8n webhook has nothing to match against. The automation skips, and the invoice remains unpaid in Xero.

You need to check your payment hygiene before committing to this build. If more than 20% of your revenue comes from manual wire transfers outside of Stripe or GoCardless, you have a reconciliation problem, not a churn prediction problem. Fix the payment rails first. Force clients onto direct debit or card mandates. Once the rails are digital, the AI orchestration can actually do its job.

Three mistakes to avoid

- Don't let your payment processor email your customers. When a payment fails, Stripe and GoCardless offer to send automated dunning emails. Turn this off. These emails look like they came from a machine, lack your brand voice, and ignore the context of the client relationship. A VIP customer who spends £50k a year should not get the same generic notice as a £20/month self-serve user. Handle the communication logic in your CRM, not your gateway.

- Don't treat card failures and bank failures as the same workflow. Cards fail because they expire, hit limits, or get flagged for fraud. Bank mandates fail primarily due to insufficient funds. If you use both Stripe and GoCardless, do not route their failure webhooks into the same generic sequence. A failed card needs an immediate prompt to the user to type in new digits. A failed direct debit needs a polite notice that you will automatically retry on a specific date. If you mix these up, you confuse the customer and delay the revenue.

- Don't leave your sales team in the dark. Once you do build a recovery workflow, you need to expose the status to the people talking to the clients. If a customer is in the middle of a 14-day retry schedule, that data must be visible on their CRM profile. If you hide the isolated AI illusion in the finance department, your sales reps will inevitably try to upsell an account that is technically in default. Push the dunning status directly into HubSpot or Pipedrive so everyone knows exactly where the account stands.

Get our UK AI insights.

Practical reads on AI for UK businesses — teardowns, how-to guides, regulatory news. Unsubscribe anytime.

Unsubscribe anytime.