Bridging the Working Capital Air Gap with Agentic Finance

You land a £120k wholesale order from a major high-street retailer. The margin is excellent. The champagne comes out. Then you look at the terms.

Net 60 days.

Meanwhile, your factory in Shenzhen wants 50% upfront to start production. You have the cash on paper, but it is entirely trapped in unpaid invoices from last month's wholesale runs. You cannot fulfil the new order without starving your operational cash flow.

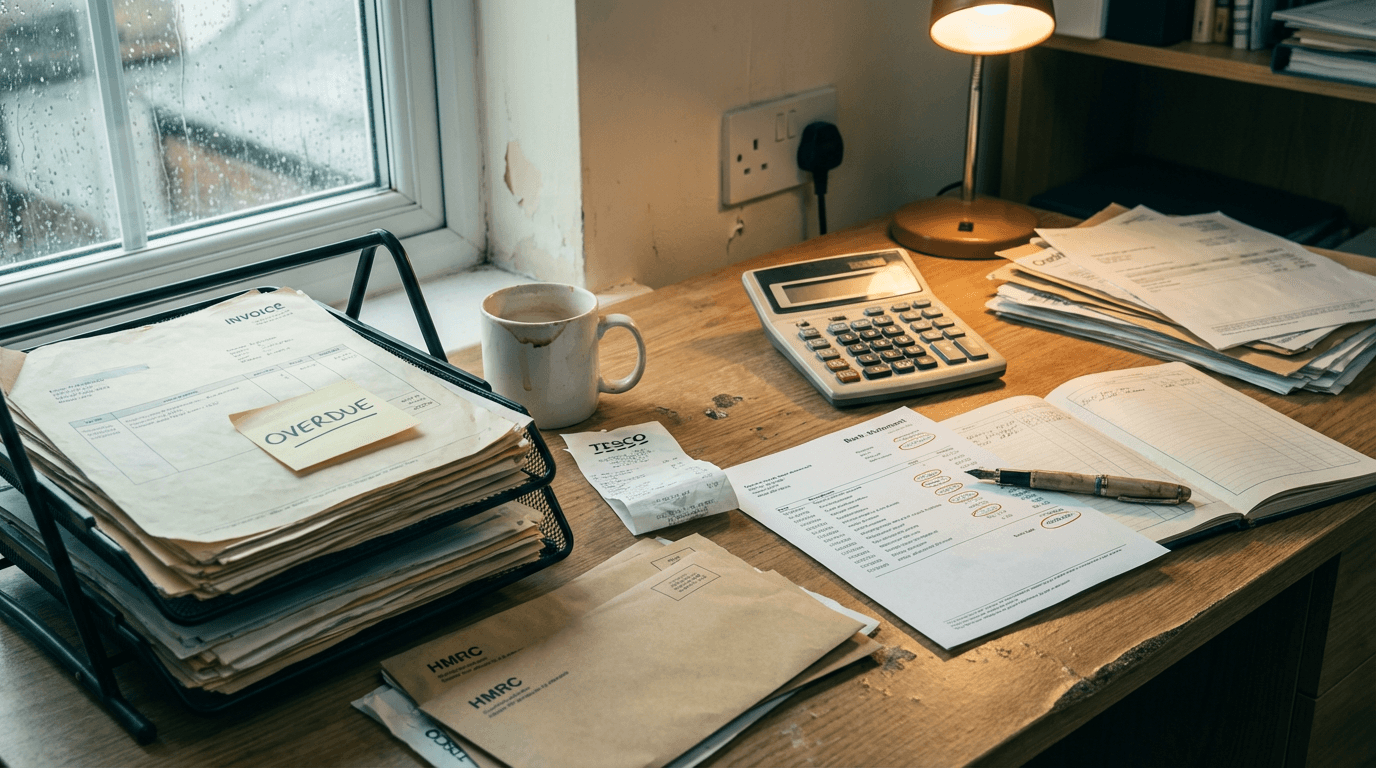

This is the exact moment growth breaks for UK consumer brands. You are profitable, but you are broke. You spend your mornings chasing accounts payable departments instead of building your business. The system is rigged against the supplier.

The working capital air gap

The working capital air gap is the critical delay between when a business must pay its suppliers for inventory and when it actually collects cash from its wholesale buyers. It is a structural flaw in modern retail, and it is quietly suffocating independent brands.

When your cash conversion cycle stretches to 90 days, you become a free credit facility for your largest customers. You absorb the upfront inventory costs. You carry the risk. They hold the cash. You end up penalised for your own success. Every new purchase order accelerates your cash burn.

This is not a niche issue. The UK SME funding gap sits at roughly £22 billion [source](https://financialit.net/news/embedded-finance/froda-and-triffin-join-forces-unlock-100-million-uk-consumer-brands). Around 60% of small firms are actively delaying investment just to rebuild liquidity [source](https://financialit.net/news/embedded-finance/froda-and-triffin-join-forces-unlock-100-million-uk-consumer-brands). Traditional banks offer no relief.

They want personal guarantees, three years of audited accounts, and six weeks to make a decision on an overdraft extension. By the time the bank says yes, you have already lost the wholesale order.

The air gap persists because legacy finance runs on batch processing and manual reconciliation. Invoices sit in inboxes. Payments clear on arbitrary runs. Nobody knows their exact cash position on a Tuesday afternoon.

So businesses hoard cash, stifle their own growth, and hope the big retailers pay on time. It is a defensive crouch that prevents aggressive scaling.

Why the obvious fix fails

Most SMEs try to solve this by duct-taping generic AI tools to their accounting software. They buy a ChatGPT Plus subscription, set up a few Zapier flows, and hope the cash collects itself.

It fails.

Zapier's Find steps can't nest, so when your Xero supplier has a custom contact field two levels deep, the automation silently writes null and you only notice at month-end. You end up with a ledger full of orphaned entries. The data structure of double-entry bookkeeping simply rejects flat, linear automation logic.

Then there is the LLM wrapper approach. You plug an AI tool into your inbox to draft polite chasing emails to late-paying clients.

A £25/month ChatGPT subscription cannot replace a £35k credit controller, and here's the mechanism: the AI has no context on the commercial relationship. It just sees an overdue flag. It will happily send a harsh legal threat to your most important anchor client over a £50 discrepancy.

More importantly, nagging emails do not create liquidity. Even if the automation works perfectly and the client promises to pay next week, you still have a cash void today. You still have to manually apply for a bank loan to bridge the gap. The automation stops exactly where the actual financial transaction needs to begin.

I see this constantly across the market. SMEs string together five different SaaS tools to predict cash flow, but when the working capital air gap actually hits, the system just throws an alert.

It tells you that you are running out of money. It does not give you the money. You are left with a very smart dashboard and a very empty bank account.

The approach that actually works

You need an agentic finance system that ties invoice parsing directly to embedded capital. This is exactly what platforms like Triffin are shipping, integrating directly with embedded lenders like Froda to deploy £100 million for UK brands [source](https://financialit.net/news/embedded-finance/froda-and-triffin-join-forces-unlock-100-million-uk-consumer-brands).

Here is what the architecture looks like when you build this out operationally.

A PDF purchase order from a major retailer hits a dedicated finance Gmail inbox. A Make webhook catches the payload and routes it to an OpenAI gpt-4o API call wrapped in a strict JSON schema. The LLM extracts the line items, quantities, and payment terms.

Crucially, you do not send this straight to your ledger. You run a deterministic Python script to validate that the sum of the extracted line items matches the invoice total. If it passes, a Make module POSTs the data to Xero to create the draft invoice.

Simultaneously, the webhook pushes the parsed data into Triffin's API. Triffin's agent evaluates the Net 60 payment term against your live bank feed and historical cash burn. It identifies a projected cash shortfall in week four.

Instead of just sending you a Slack alert, the agent automatically pings the Froda embedded lending API. It packages your historical Xero data and the verified invoice as collateral.

Froda's decision engine underwrites the risk in one minute. You click a button in Triffin, and Froda disburses the funds instantly [source](https://financialit.net/news/embedded-finance/froda-and-triffin-join-forces-unlock-100-million-uk-consumer-brands).

To build the custom routing, webhooks, and API validation layers yourself, expect 2-3 weeks of build time and £6k-£12k in development costs. That is before you even switch on the capital facility.

The most common failure mode here is hallucinated line items on multi-page PDFs. The LLM gets confused by shipping terms or discount codes and invents a new product row.

You catch this by enforcing strict schema outputs and failing the webhook if the math does not balance perfectly. The human only steps in when the script flags an error. The rest of the time, the system runs silently in the background, turning static invoices into liquid capital.

Where this breaks down

This architecture is powerful, but it requires pristine data. You need to know exactly when it will fail before you trust it with your company's cash.

If your invoices come in as scanned TIFFs from legacy accounting systems, you need an OCR layer first. Once you rely on OCR for blurry scans, the error rate jumps from 1% to ~12%.

The deterministic math validation will catch the errors, but your human-in-the-loop queue will blow up, defeating the point of the automation. You will spend more time fixing OCR typos than you would have spent manually entering the invoices.

It also breaks down if your wholesale buyers constantly dispute line items or return goods. Embedded lenders rely on predictable repayment. If a retailer routinely short-pays an invoice by 20% due to damaged stock, the automated reconciliation fails.

The AI agent expects a £10,000 settlement to clear the loan. When only £8,000 lands in the bank feed, the system cannot automatically resolve the discrepancy. You have to manually intervene to settle the outstanding debt.

Do not deploy agentic capital if your core fulfillment operations are messy. Fix the physical logistics before you automate the financial ones.

Three mistakes to avoid

If you are moving towards agentic finance, the execution is everything. Avoid these traps.

- DON'T let an LLM send unreviewed chasing emails to your biggest clients.

- DON'T use Zapier for complex nested accounting data.

- DON'T try to automate a broken credit control process.

You will ruin relationships. LLMs lack commercial nuance. They do not know that the buyer's accounts payable manager was on annual leave, or that you verbally agreed to a two-week extension over drinks. If you automate outbound communications, route the drafted emails to a Slack channel for a human to approve with a single click. Never give an agent direct send permissions on your main domain.

Get our UK AI insights.

Practical reads on AI for UK businesses — teardowns, how-to guides, regulatory news. Unsubscribe anytime.

Unsubscribe anytime.